ga_ma_2022 <- read_csv("../data/output/ma-snippets/ga-ma-data-2022.csv") %>%

group_by(fips) %>%

mutate(

total_ma_enrollment = first(avg_enrolled),

ma_share = if_else(

total_ma_enrollment > 0,

(avg_enrollment / total_ma_enrollment) * 100,

NA_real_

)

) %>%

summarize(

hhi_ma = sum(ma_share^2, na.rm = TRUE),

plan_count = n_distinct(contractid, planid),

avg_premium_partc = mean(premium_partc, na.rm = TRUE),

share_pos_premiums = mean(premium_partc > 0, na.rm = TRUE),

avg_bid = mean(bid, na.rm = TRUE),

avg_eligibles = first(avg_eligibles),

ffs_cost = first(avg_ffscost)

) %>%

ungroup()Matching and Weighting IRL

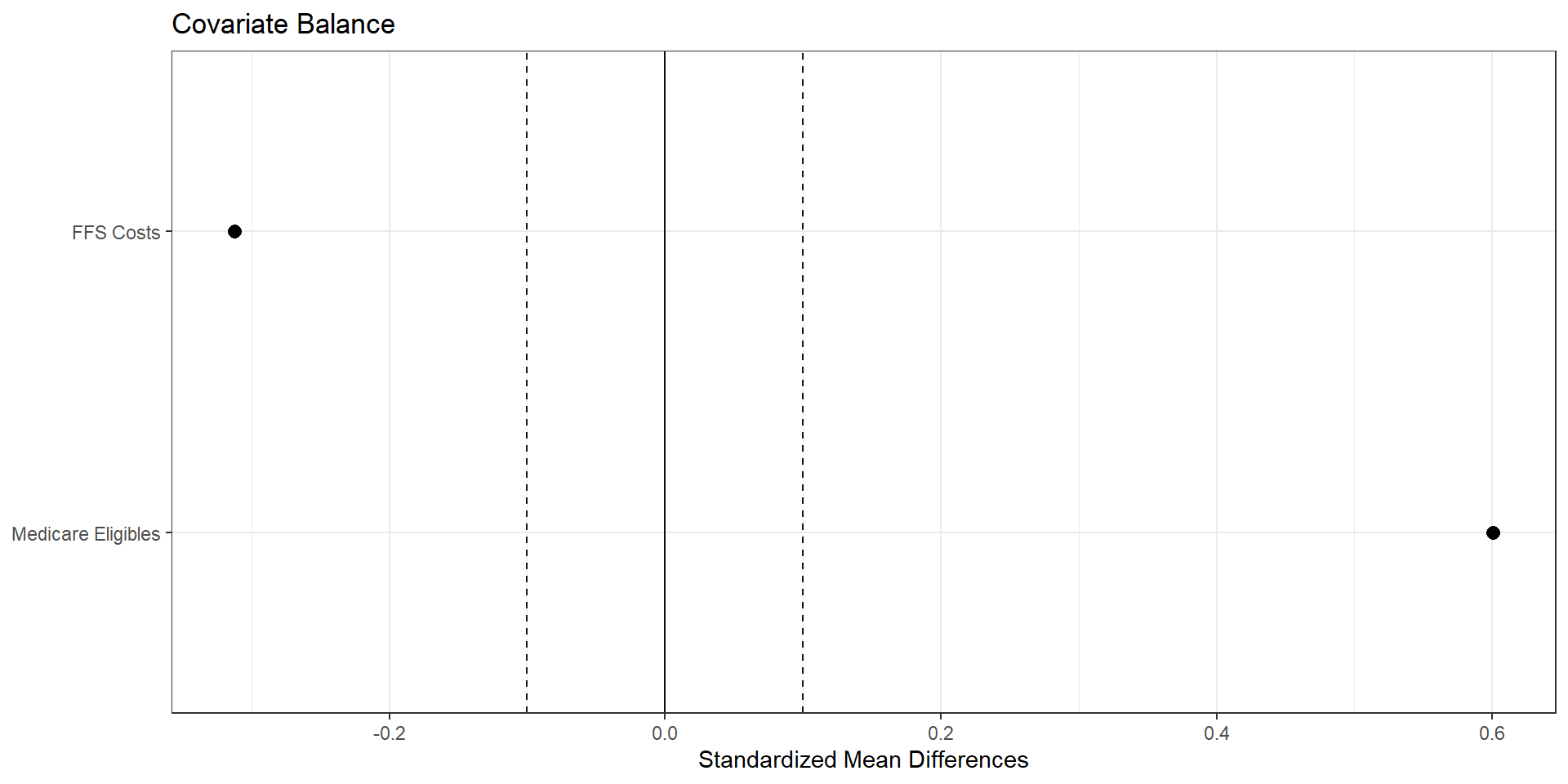

Assessing Balance

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

covariates = [

"avg_eligibles",

"ffs_cost",

]

lp_vars = ga_tab[["hhi_group"] + covariates].dropna()

treated = lp_vars[lp_vars["hhi_group"] == "treated"]

control = lp_vars[lp_vars["hhi_group"] == "control"]

# -------------------------------------------------------------------

# Standardized mean differences (treated – control)

# SMD = (m1 - m0) / sqrt((s1^2 + s0^2)/2)

# -------------------------------------------------------------------

def smd(x_t, x_c):

m1, m0 = x_t.mean(), x_c.mean()

v1, v0 = x_t.var(ddof=1), x_c.var(ddof=1)

return (m1 - m0) / np.sqrt((v1 + v0) / 2)

smd_list = []

for var in covariates:

smd_val = smd(treated[var], control[var])

smd_list.append({"variable": var, "smd": smd_val})

smd_df = pd.DataFrame(smd_list)

smd_df["abs_smd"] = smd_df["smd"].abs()

# Optional: nicer labels

rename_map = {

"avg_eligibles" : "Avg eligibles",

"ffs_cost" : "Avg FFS cost",

}

smd_df["label"] = smd_df["variable"].replace(rename_map)

# Sort by absolute SMD for a nicer plot

smd_df = smd_df.sort_values("abs_smd")

# -------------------------------------------------------------------

# “Love plot” using matplotlib

# -------------------------------------------------------------------

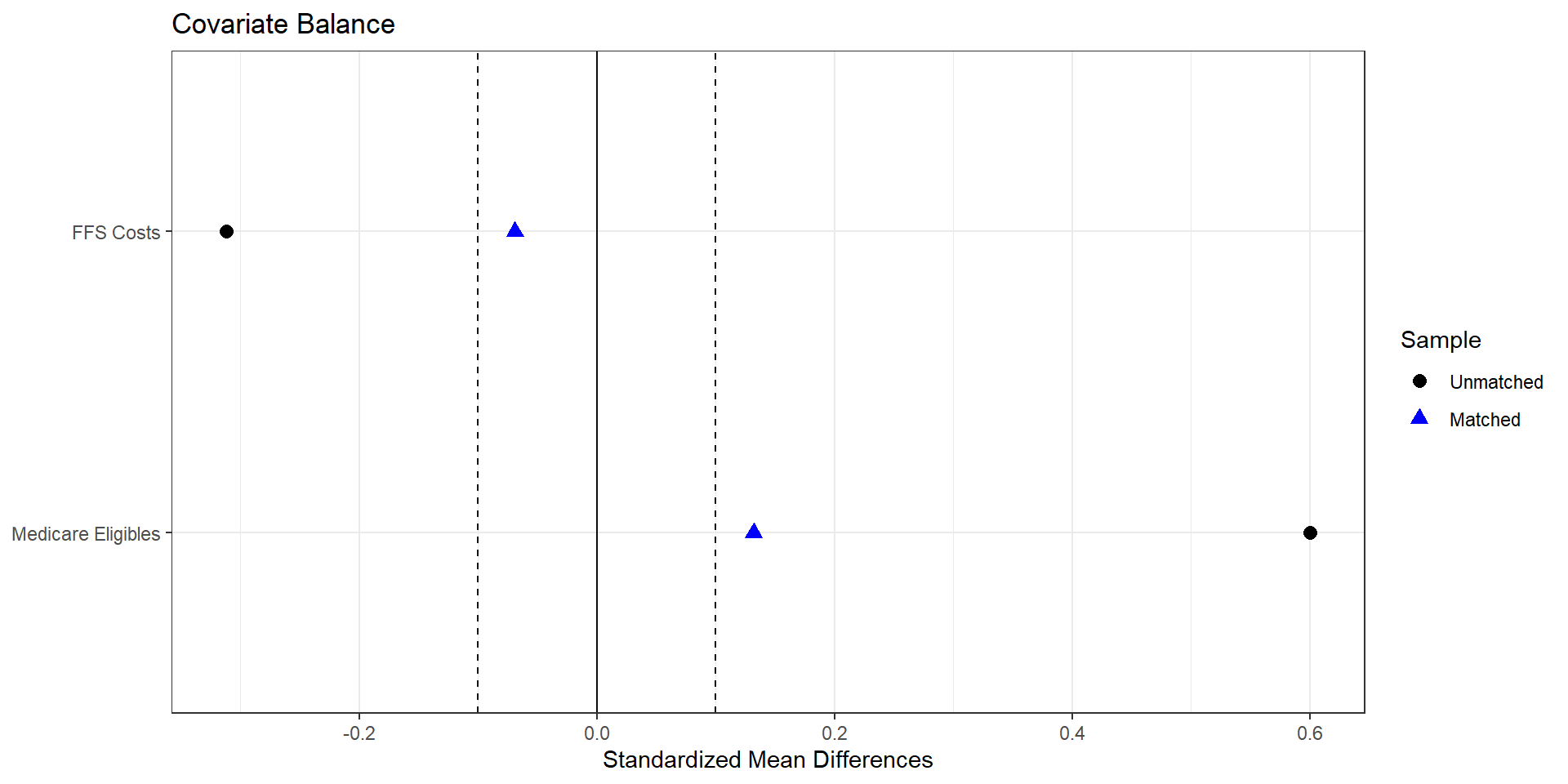

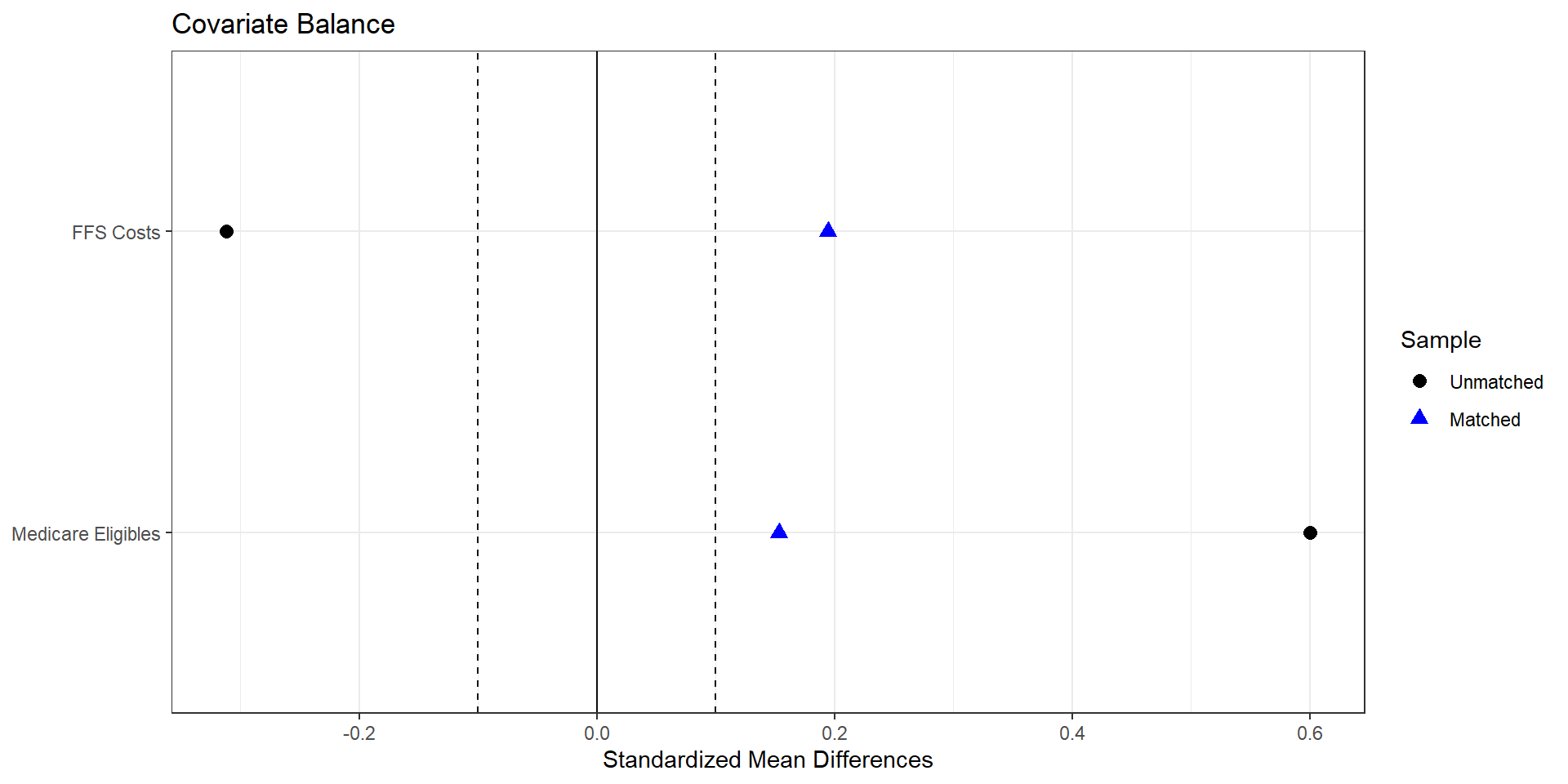

fig, ax = plt.subplots(figsize=(6, 4))

ax.scatter(smd_df["smd"], smd_df["label"])

# Reference lines at 0 and +/- 0.1

ax.axvline(0.0, color="black", linewidth=1)

ax.axvline(0.1, color="grey", linestyle="--", linewidth=1)

ax.axvline(-0.1, color="grey", linestyle="--", linewidth=1)

ax.set_xlabel("Standardized mean difference (treated - control)")

ax.set_ylabel("Covariate")

ax.set_title("Covariate balance by HHI treatment status")

plt.tight_layout()

plt.show()

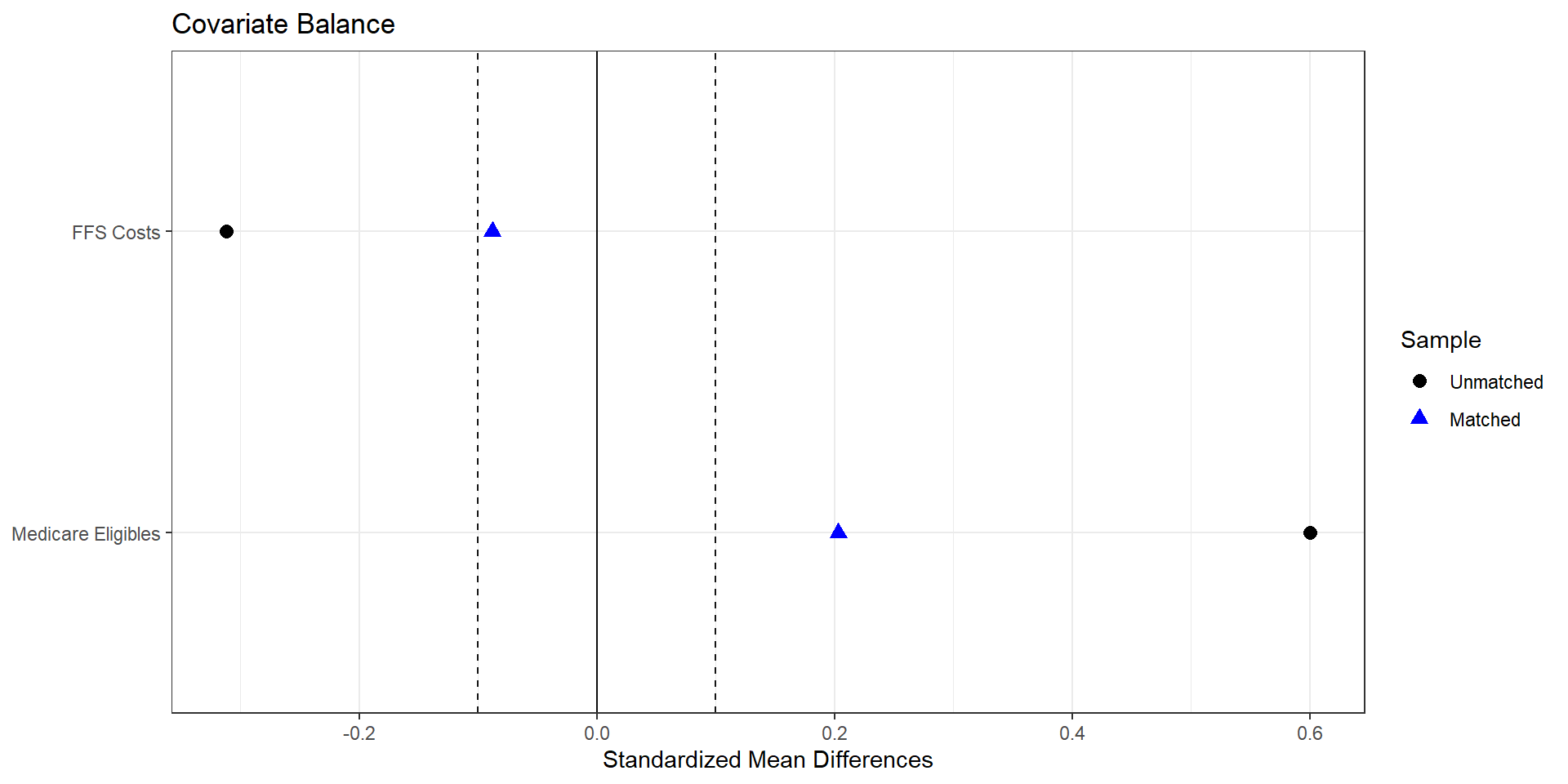

1. Exact Matching (on a subset)

2. Nearest neighbor matching (inverse variance, many matches)

import numpy as np

import pandas as pd

from sklearn.preprocessing import StandardScaler

from sklearn.neighbors import NearestNeighbors

# lp_df should contain:

# - 'avg_bid' (outcome, like Y)

# - 'treated_dummy' (0/1, like Tr)

# - all columns in lp.covs (covariates for matching)

cov_cols = [

"avg_eligibles",

"ffs_cost",

]

# Drop missing

lp_df_cc = lp_df.dropna(subset=cov_cols + ["avg_bid", "treated_dummy"]).copy()

treated = lp_df_cc[lp_df_cc["treated_dummy"] == 1].copy()

controls = lp_df_cc[lp_df_cc["treated_dummy"] == 0].copy()

X_t = treated[cov_cols].values

X_c = controls[cov_cols].values

y_t = treated["avg_bid"].values

y_c = controls["avg_bid"].values

# Standardize covariates (rough analogue to Weight=1 / inverse-variance scaling)

scaler = StandardScaler()

X_c_scaled = scaler.fit_transform(X_c)

X_t_scaled = scaler.transform(X_t)

# Nearest neighbors: M = 4 matches per treated

M = 4

nn = NearestNeighbors(n_neighbors=M, metric="euclidean")

nn.fit(X_c_scaled)

distances, indices = nn.kneighbors(X_t_scaled, return_distance=True)

# For each treated unit, average its matched controls' outcomes

matched_ctrl_means = y_c[indices].mean(axis=1)

# ATT-style estimate: E[Y(1) - Y(0) | treated]

effect_nn = np.mean(y_t - matched_ctrl_means)

print("Nearest-neighbor estimate for avg_bid (treated - control):", effect_nn)

Estimate... 11.133

AI SE...... 3.7953

T-stat..... 2.9333

p.val...... 0.003354

Original number of observations.............. 107

Original number of treated obs............... 54

Matched number of observations............... 107

Matched number of observations (unweighted). 428 2. Nearest neighbor matching (inverse variance, one-to-one)

import numpy as np

import pandas as pd

from sklearn.preprocessing import StandardScaler

from sklearn.neighbors import NearestNeighbors

# lp_df should contain:

# - 'avg_bid' (outcome, like Y)

# - 'treated_dummy' (0/1, like Tr)

# - all columns in lp.covs (covariates for matching)

cov_cols = [

"avg_eligibles",

"ffs_cost",

]

# Drop missing

lp_df_cc = lp_df.dropna(subset=cov_cols + ["avg_bid", "treated_dummy"]).copy()

treated = lp_df_cc[lp_df_cc["treated_dummy"] == 1].copy()

controls = lp_df_cc[lp_df_cc["treated_dummy"] == 0].copy()

X_t = treated[cov_cols].values

X_c = controls[cov_cols].values

y_t = treated["avg_bid"].values

y_c = controls["avg_bid"].values

# Standardize covariates (rough analogue to Weight=1 / inverse-variance scaling)

scaler = StandardScaler()

X_c_scaled = scaler.fit_transform(X_c)

X_t_scaled = scaler.transform(X_t)

# Nearest neighbors: M = 1 match per treated

M = 1

nn = NearestNeighbors(n_neighbors=M, metric="euclidean")

nn.fit(X_c_scaled)

distances, indices = nn.kneighbors(X_t_scaled, return_distance=True)

# For each treated unit, average its matched controls' outcomes

matched_ctrl_means = y_c[indices].mean(axis=1)

# ATT-style estimate: E[Y(1) - Y(0) | treated]

effect_nn = np.mean(y_t - matched_ctrl_means)

print("Nearest-neighbor estimate for avg_bid (treated - control):", effect_nn)

Estimate... 11.726

AI SE...... 4.3248

T-stat..... 2.7114

p.val...... 0.0067009

Original number of observations.............. 107

Original number of treated obs............... 54

Matched number of observations............... 107

Matched number of observations (unweighted). 107 2. Nearest neighbor matching (Mahalanobis)

import numpy as np

import pandas as pd

from sklearn.neighbors import NearestNeighbors

# Covariate set X (matching variables)

cov_cols = [

"avg_eligibles",

"ffs_cost",

]

# Drop missing on outcome / treatment / covariates

lp_df_cc = lp_df.dropna(subset=cov_cols + ["avg_bid", "treated_dummy"]).copy()

treated = lp_df_cc[lp_df_cc["treated_dummy"] == 1].copy()

controls = lp_df_cc[lp_df_cc["treated_dummy"] == 0].copy()

X_t = treated[cov_cols].to_numpy()

X_c = controls[cov_cols].to_numpy()

y_t = treated["avg_bid"].to_numpy()

y_c = controls["avg_bid"].to_numpy()

# Pooled covariance of covariates (R's Matching uses Mahalanobis on X)

V = np.cov(np.vstack([X_t, X_c]).T)

# 1-nearest neighbor with Mahalanobis distance --------------------------

nn = NearestNeighbors(

n_neighbors=1,

metric="mahalanobis",

metric_params={"V": V}

)

nn.fit(X_c)

distances, indices = nn.kneighbors(X_t, return_distance=True)

# Matched control outcomes

matched_ctrl = y_c[indices.flatten()]

# ATT-style effect (treated minus matched controls)

effect_nn_md = np.mean(y_t - matched_ctrl)

print("Mahalanobis 1-NN estimate for avg_bid (treated - control):", effect_nn_md)

Estimate... 11.416

AI SE...... 4.3543

T-stat..... 2.6217

p.val...... 0.0087482

Original number of observations.............. 107

Original number of treated obs............... 54

Matched number of observations............... 107

Matched number of observations (unweighted). 107 2. Nearest neighbor matching (propensity score)

import numpy as np

import pandas as pd

import statsmodels.formula.api as smf

from sklearn.neighbors import NearestNeighbors

# lp_df should contain:

# - 'avg_bid' (outcome)

# - 'treated_dummy' (0/1)

# - 'avg_eligibles'

# - 'ffs_cost' # use 'ffs_cost' here if that's your column name

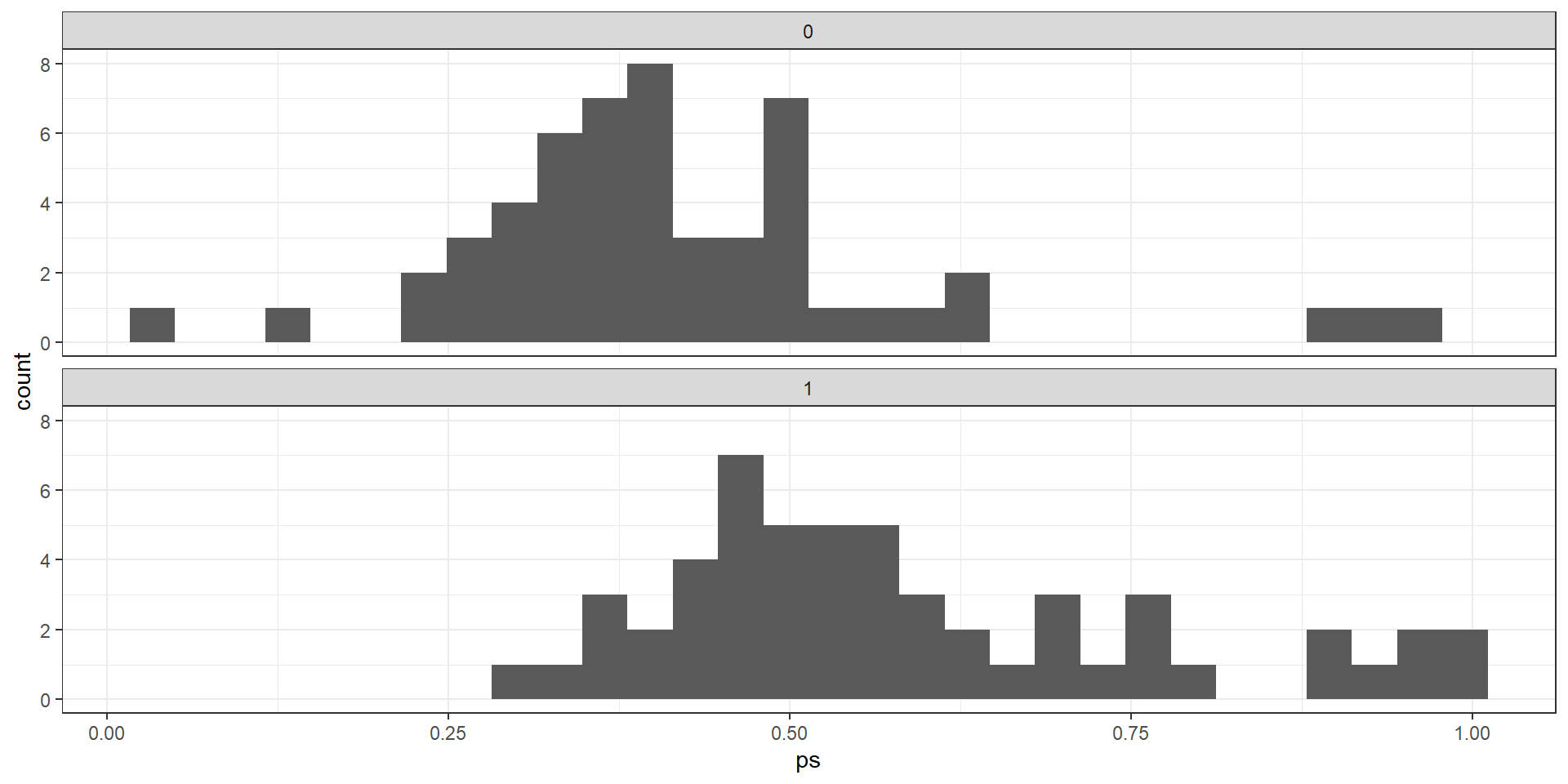

# 1. Estimate propensity scores ----------------------------------------

logit_res = smf.logit(

"treated_dummy ~ avg_eligibles + ffs_cost",

data=lp_df

).fit()

lp_df_ps = lp_df.copy()

lp_df_ps["ps"] = logit_res.predict(lp_df_ps)

# Optional: trim extreme PS

eps = 1e-6

lp_df_ps["ps"] = lp_df_ps["ps"].clip(eps, 1 - eps)

# 2. Prepare treated / control samples ---------------------------------

lp_df_cc = lp_df_ps.dropna(subset=["avg_bid", "treated_dummy", "ps"]).copy()

treated = lp_df_cc[lp_df_cc["treated_dummy"] == 1].copy()

controls = lp_df_cc[lp_df_cc["treated_dummy"] == 0].copy()

y_t = treated["avg_bid"].to_numpy()

y_c = controls["avg_bid"].to_numpy()

X_t = treated[["ps"]].to_numpy() # 1D propensity score as matching covariate

X_c = controls[["ps"]].to_numpy()

# 3. 1-nearest neighbor on propensity score (ATT-style) ----------------

nn = NearestNeighbors(n_neighbors=1, metric="euclidean")

nn.fit(X_c)

distances, indices = nn.kneighbors(X_t, return_distance=True)

matched_ctrl = y_c[indices.flatten()]

effect_ps_nn = np.mean(y_t - matched_ctrl)

print("PS 1-NN estimate for avg_bid (treated - control):", effect_ps_nn)

Estimate... 13.097

AI SE...... 4.6112

T-stat..... 2.8402

p.val...... 0.0045081

Original number of observations.............. 107

Original number of treated obs............... 54

Matched number of observations............... 107

Matched number of observations (unweighted). 108 3. Weighting with Simple Averages

lp.vars <- lp.vars %>%

mutate(ipw = case_when(

treated_dummy==1 ~ 1/ps,

treated_dummy==0 ~ 1/(1-ps),

TRUE ~ NA_real_

))

mean.t1 <- lp.vars %>% filter(treated_dummy==1) %>%

select(avg_bid, ipw) %>% summarize(mean_bid=weighted.mean(avg_bid,w=ipw))

mean.t0 <- lp.vars %>% filter(treated_dummy==0) %>%

select(avg_bid, ipw) %>% summarize(mean_bid=weighted.mean(avg_bid,w=ipw))import numpy as np

import pandas as pd

p_vars = lp_df.copy()

# Inverse probability weights

p_vars["ipw"] = np.where(

p_vars["treated_dummy"] == 1,

1.0 / p_vars["ps"],

1.0 / (1.0 - p_vars["ps"])

)

# Treated group weighted mean of avg_bid

treated = p_vars[p_vars["treated_dummy"] == 1]

mean_t1 = np.average(treated["avg_bid"], weights=treated["ipw"])

# Control group weighted mean of avg_bid

controls = p_vars[p_vars["treated_dummy"] == 0]

mean_t0 = np.average(controls["avg_bid"], weights=controls["ipw"])

ate_ipw = mean_t1 - mean_t0

print("IPW mean (treated):", mean_t1)

print("IPW mean (control):", mean_t0)

print("IPW ATE (treated - control):", ate_ipw)

[1] 6.301051