Regression Discontinuity: Part II

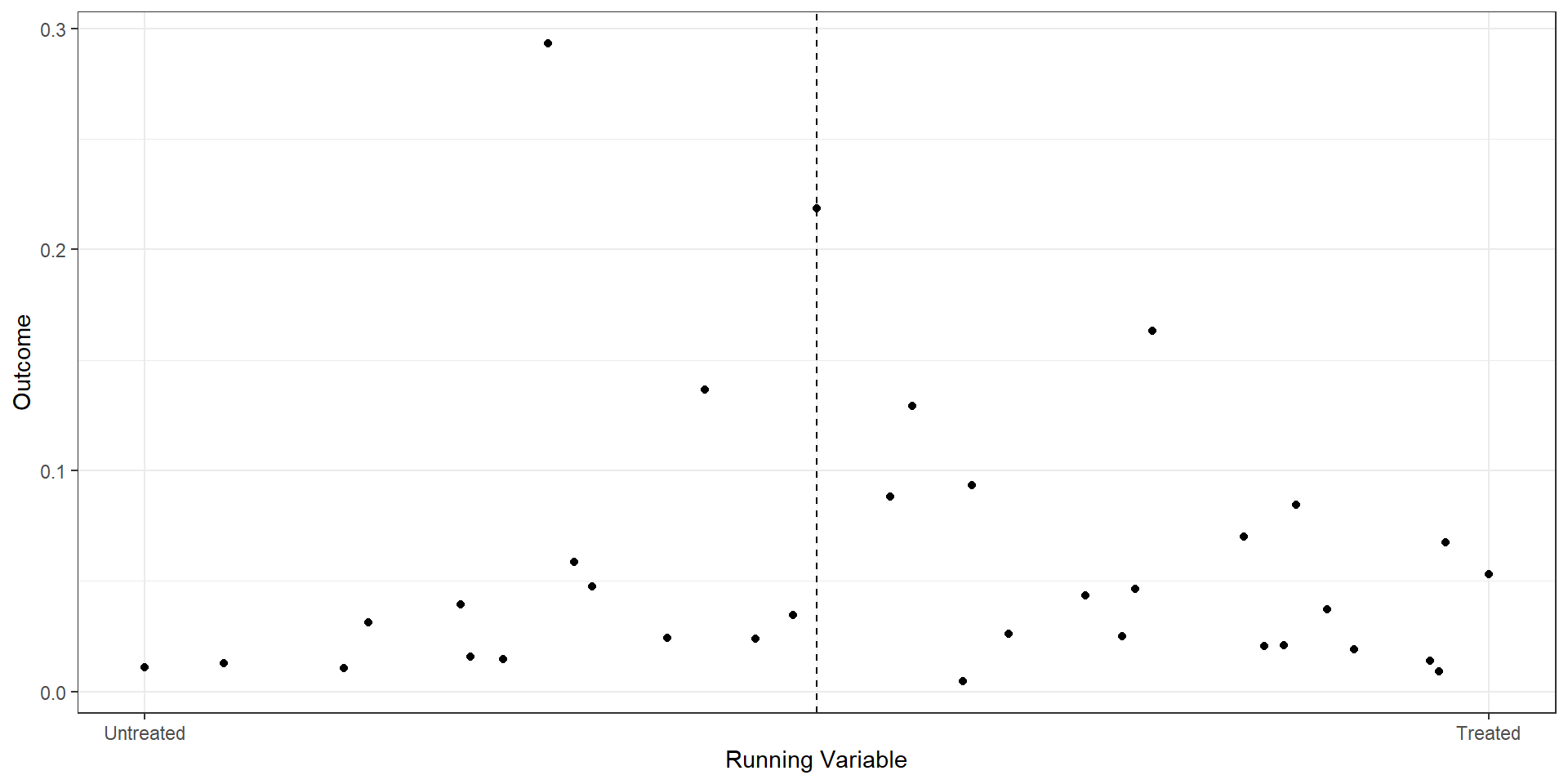

Binned Scatterplot

rd.result <- rdplot(ma_25star$mkt_share, ma_25star$raw_rating,

c=2.25, p=2,

title="RD Plot with Binned Average",

x.label="Running Variable",

y.label="Outcome",

hide = TRUE)

bin.avg <- as_tibble(rd.result$vars_bins)

plot.bin <- bin.avg %>% ggplot(aes(x=rdplot_mean_x,y=rdplot_mean_y)) +

geom_point() + theme_bw() +

geom_vline(aes(xintercept=2.25),linetype='dashed') +

scale_x_continuous(

breaks = c(2, 2.125, 2.25, 2.375, 2.5),

label = c("2.0", "2.125", "2.25", "2.375", "2.5")

) +

xlab("Raw Rating") + ylab("Market Share") +

annotate("text", x=2.25, y=Inf, label="2.5-star\ncutoff",

vjust=1.5, hjust=-0.1, size=3.5, color="grey40")import pandas as pd

import matplotlib.pyplot as plt

from rdrobust import rdplot

# RD plot using mkt_share as outcome and raw_rating as running variable

rd_result = rdplot(

y=ma_25star["mkt_share"].values,

x=ma_25star["raw_rating"].values,

c=2.25,

title="RD Plot with Binned Average",

x_label="Running Variable",

y_label="Outcome",

hide=True # don't show the built-in plot

)

# vars_bins is already a pandas DataFrame in the Python implementation

bin_avg = rd_result.vars_bins

# Recreate the custom plot

fig, ax = plt.subplots()

ax.scatter(

bin_avg["rdplot_mean_x"],

bin_avg["rdplot_mean_y"]

)

ax.axvline(x=2.25, linestyle="--", color="grey")

ax.set_xticks([2.0, 2.125, 2.25, 2.375, 2.5])

ax.set_xticklabels(["2.0", "2.125", "2.25", "2.375", "2.5"])

ax.set_xlabel("Raw Rating")

ax.set_ylabel("Market Share")

ax.set_title("RD Plot with Binned Average")

ax.annotate("2.5-star\ncutoff", xy=(2.25, ax.get_ylim()[1]),

xytext=(2.27, ax.get_ylim()[1]*0.95), fontsize=9, color="grey")

plt.tight_layout()

plt.show()

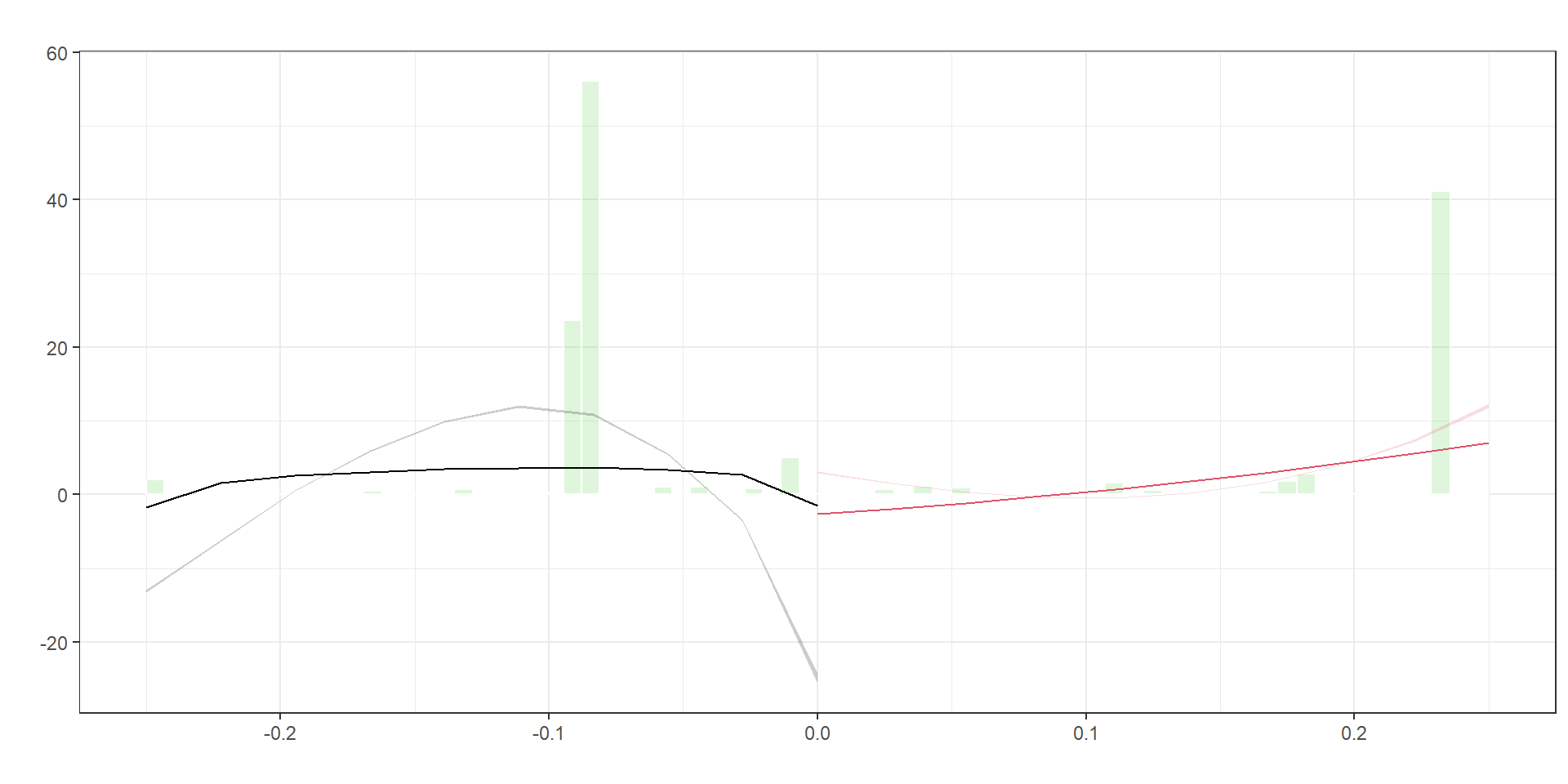

Manipulation of the running variable

from rdrobust import rddensity, rdplotdensity

import matplotlib.pyplot as plt

# Run McCrary-style density test at cutoff 0

dens1 = rddensity(x=ma_rd1["score"].values, c=0)

# Create the density plot object (rdplotdensity returns a matplotlib figure/axes)

densplot = rdplotdensity(dens1, x=ma_rd1["score"].values)

# If you want to explicitly show or tweak:

fig = densplot["fig"]

ax = densplot["ax"]

ax.set_title("Density test around cutoff")

ax.set_xlabel("Score")

ax.set_ylabel("Estimated density")

plt.show()| Value | |

|---|---|

| T-statistic | 55.91 |

| P-value | 0.00 |

Interpretation: A large p-value means we cannot reject equal density on both sides of the cutoff, which is what we want. No evidence of manipulation.

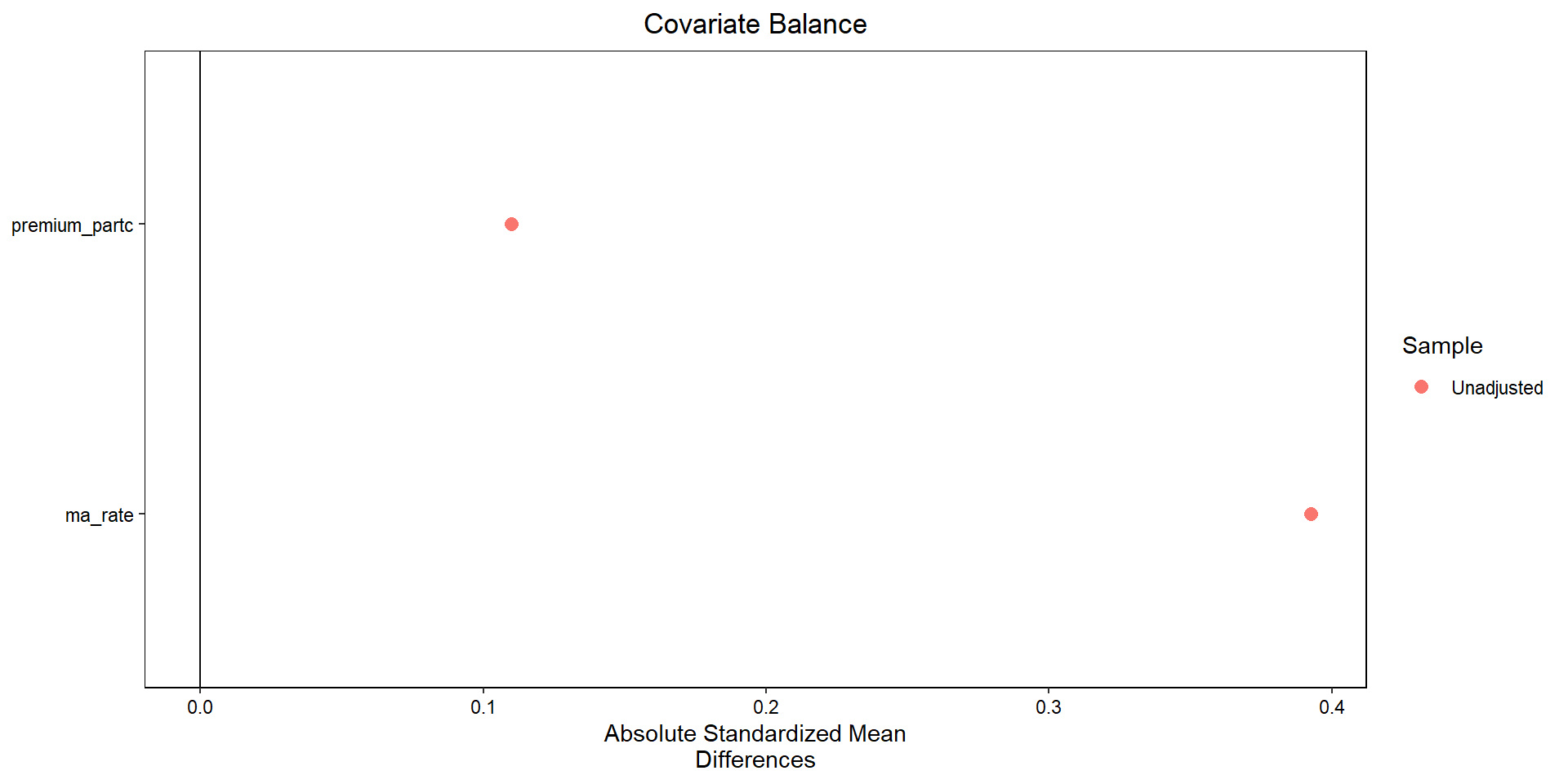

Covariate balance

import numpy as np

import pandas as pd

from sklearn.neighbors import NearestNeighbors

import matplotlib.pyplot as plt

# 1. Subset data as in your R code

sub = (

ma_rd1

.loc[

(ma_rd1["window2"]) &

ma_rd1["treat"].notna() &

ma_rd1["premium_partc"].notna() &

ma_rd1["ma_rate"].notna()

]

.copy()

)

covariates = ["premium_partc", "ma_rate"]

X = sub[covariates].to_numpy()

t = sub["treat"].astype(int).to_numpy()

# 2. Mahalanobis nearest-neighbor matching (1:1)

# Estimate covariance matrix of covariates and its inverse

V = np.cov(X, rowvar=False)

V_inv = np.linalg.inv(V)

# Fit NN on controls only

nn = NearestNeighbors(

n_neighbors=1,

metric="mahalanobis",

metric_params={"V": V}

)

nn.fit(X[t == 0])

# For each treated unit, find nearest control

dist, idx = nn.kneighbors(X[t == 1])

control_matches = sub.loc[t == 0].iloc[idx[:, 0]].copy()

treated_matched = sub.loc[t == 1].copy()

# Build matched sample

matched = pd.concat(

[

treated_matched.reset_index(drop=True),

control_matches.reset_index(drop=True)

],

axis=0

).reset_index(drop=True)

matched["treat"] = np.r_[np.ones(len(treated_matched)), np.zeros(len(control_matches))]

# 3. Function for standardized mean differences (SMD)

def smd(df, var, treat_col="treat"):

g1 = df[df[treat_col] == 1][var]

g0 = df[df[treat_col] == 0][var]

m1, m0 = g1.mean(), g0.mean()

s = np.sqrt(0.5 * (g1.var(ddof=1) + g0.var(ddof=1)))

return (m1 - m0) / s

# SMDs before and after matching

smd_before = [smd(sub, v) for v in covariates]

smd_after = [smd(matched, v) for v in covariates]

# 4. “Love plot” (absolute SMDs)

fig, ax = plt.subplots()

y_pos = np.arange(len(covariates))

ax.scatter(np.abs(smd_before), y_pos, marker="o", label="Unmatched")

ax.scatter(np.abs(smd_after), y_pos, marker="s", label="Matched")

ax.set_yticks(y_pos)

ax.set_yticklabels(covariates)

ax.set_xlabel("Absolute standardized mean difference")

ax.axvline(0.1, linestyle="--") # common reference line

ax.legend()

ax.invert_yaxis() # to mimic cobalt’s ordering

plt.tight_layout()

plt.show()

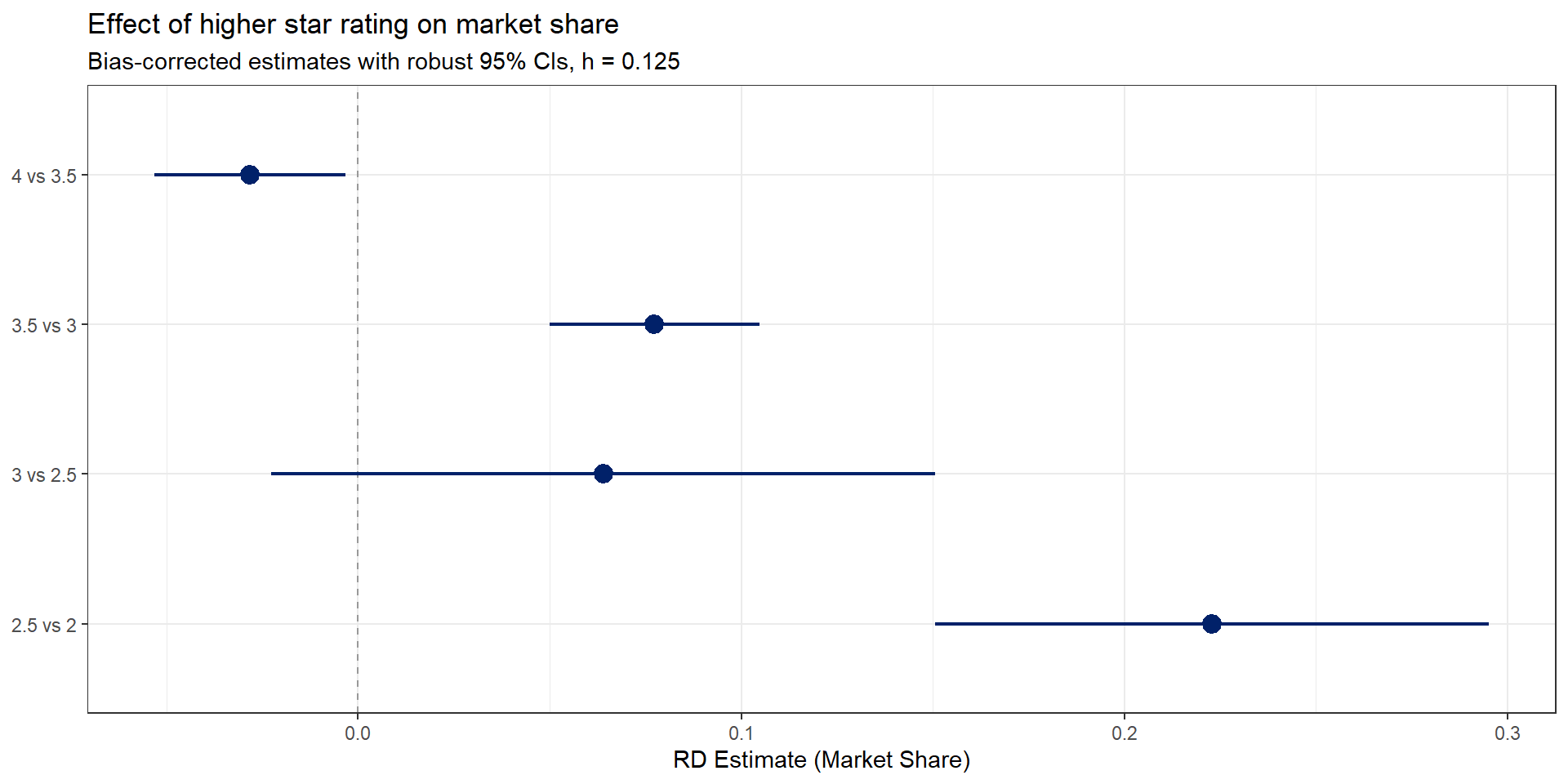

Effects across all thresholds

Same approach, applied to every half-star cutoff. The code below loops over each threshold and collects the rdrobust estimates into a single data frame.

cutoffs <- tibble(

lower = c(2, 2.5, 3, 3.5),

upper = c(2.5, 3, 3.5, 4),

cutoff = c(2.25, 2.75, 3.25, 3.75)

)

rd_results <- cutoffs %>%

pmap_dfr(function(lower, upper, cutoff) {

dat <- ma_2009 %>%

filter(Star_Rating == lower | Star_Rating == upper) %>%

mutate(score = raw_rating - cutoff)

est <- rdrobust(y=dat$mkt_share, x=dat$score, c=0,

h=0.125, p=1, kernel="uniform", vce="hc0",

masspoints="off")

tibble(

threshold = paste0(upper, " vs ", lower),

estimate = est$coef[2],

ci_lower = est$ci[3,1],

ci_upper = est$ci[3,2],

n = est$N[1] + est$N[2]

)

})from rdrobust import rdrobust

import pandas as pd

cutoffs = [

(2, 2.5, 2.25),

(2.5, 3, 2.75),

(3, 3.5, 3.25),

(3.5, 4, 3.75),

]

results = []

for lower, upper, cutoff in cutoffs:

dat = ma_2009[ma_2009["Star_Rating"].isin([lower, upper])].copy()

dat["score"] = dat["raw_rating"] - cutoff

est = rdrobust(

y=dat["mkt_share"].values,

x=dat["score"].values,

c=0, h=0.125, p=1,

kernel="uniform", vce="hc0",

masspoints="off"

)

results.append({

"threshold": f"{upper} vs {lower}",

"estimate": est.coef.iloc[1, 0], # bias-corrected

"ci_lower": est.ci.iloc[2, 0], # robust CI

"ci_upper": est.ci.iloc[2, 1],

})

rd_results = pd.DataFrame(results)